Summary

Computer Modelling Groups fiscal fourth quarter of 2025 saw the stock react with an ~18% drop following the earnings release, as the market digested some poor organic growth due to customer churn in the core business as well as a not so rosy outlook for 2026 organically. After two years of significant growth in the reservoir and production solutions, CMG has encountered a setback this year. Growth historically was fueled by acquiring new customers, expanding services with existing clients, and making strides in Energy Transition, especially in Carbon Capture & Storage (CCS).

However, two key factors have shifted the landscape:

Declining oil prices have impacted the industry. Customers, particularly smaller and medium-sized operators, are tightening budgets and scrutinizing technology spending more closely, which led to churn in Q4.

Many companies are re-evaluating their energy transition and renewable strategies. Carbon Capture & Storage (CCS), which saw a surge in momentum due to U.S. Inflation Reduction Act tax incentives, has now slowed down considerably, leading to a noticeable pullback in U.S. activity (14% decline in US geographic revenue).

The fourth quarter of 2025 saw total revenue rise by 4% to $33.7 million, primarily driven by a 17% increase from acquisitions, which helped offset a 13% organic decline. Recurring revenue also grew by 16% to $24.2 million, with acquisitions contributing 23% growth despite a 7% organic decline. Adjusted EBITDA increased by 2% to $10.5 million, though the adjusted EBITDA margin slightly decreased to 31% from 32% in the prior year. However, earnings per share fell by 33% to $0.06, and free cash flow decreased by 26% to $7.0 million, resulting in a per-share decline to $0.08 from $0.12.

For the full fiscal year 2025, total revenue saw a significant 19% increase to $129.4 million, largely due to a 20% growth from acquisitions, which compensated for a 1% organic decline. Recurring revenue also increased by 13% to $86.8 million, with 12% of that growth stemming from acquisitions and a modest 1% organic growth. Adjusted EBITDA rose by 2% to $44.0 million, though the adjusted EBITDA margin decreased to 34% from 40% in the comparative period. Earnings per share for the fiscal year decreased by 16% to $0.27, and free cash flow declined by 22% to $27.6 million, with free cash flow per share dropping to $0.33 from $0.44.

Looking ahead to fiscal year 2026, management is anticipating a decrease of $6 to $7 million in professional services revenue compared to fiscal 2025, assuming no new acquisitions. Additionally, investors should expect to see limited growth in Adjusted EBITDA and Adjusted EBITDA Margin.

On a more positive note CMG's two most recent acquisitions are performing well in terms of revenue and profit margins. Having successfully integrated two acquisitions and deployed 95% of free cash flow over the past two years, CMG appears more ready to accelerate the acquisition strategy. The company has expanded its acquisition focus beyond its traditional market to include midstream, downstream, and related sectors like utilities and mining and from our research could be exploring new verticals such as automotive and aerospace.

Moving forward, our investment depends entirely on management's ability to execute successful mergers and acquisitions. If these M&A activities expand the company into new sectors, it will stabilize organic growth through diversification and align with our initial investment expectations below.

Investment Thesis

Oil & Gas Industry Turning to Software to Lower Costs

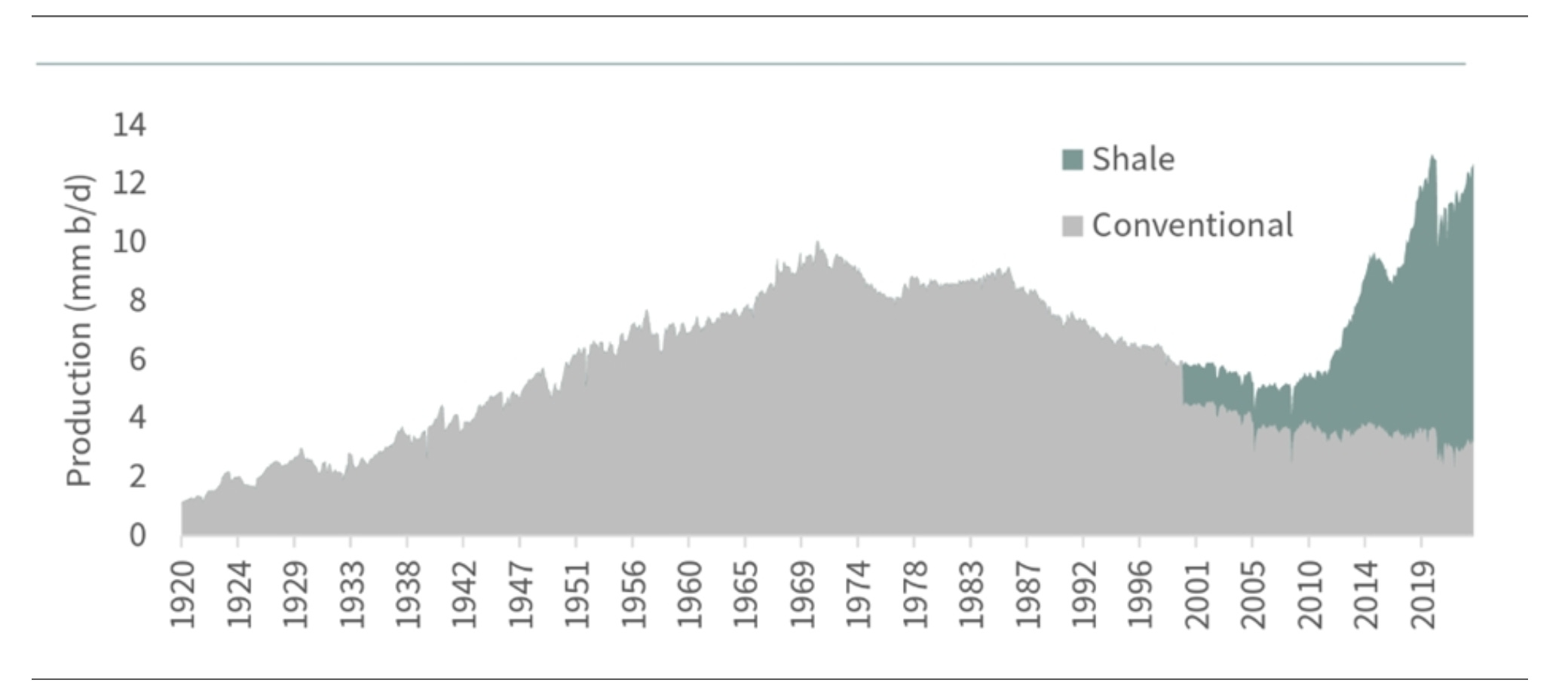

The decline in conventional petroleum production over the past decade has been exacerbated by the complexities of shale oil and gas extraction. To address these challenges, the industry has increasingly turned to software and automation to streamline once-simple mechanical processes. As commodity prices fluctuate, companies have focused on improving efficiency and reducing operating costs. To achieve these goals, they are relying more heavily on software simulations to optimize production. CMG, with its decades of experience in reservoir simulation software and strong market presence, is a leader in this evolving landscape.

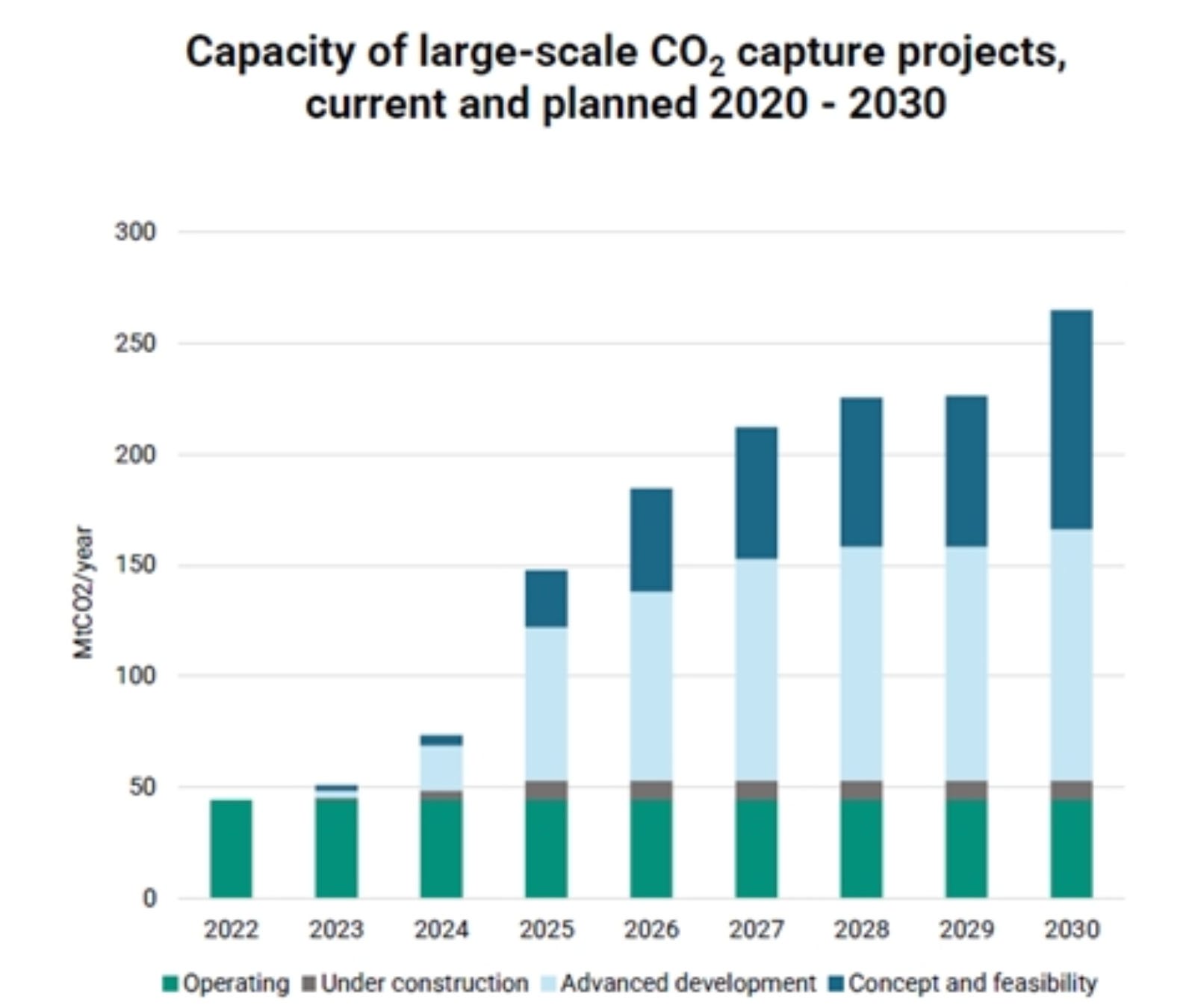

Organic Growth Opportunities in Carbon Capture & Storage

CMG has been strategically expanding into the energy transition market, focusing on carbon capture and storage (CCS). As the CCS industry continues to grow, driven by government incentives and a global push for net carbon neutrality, CMG is well-positioned to capitalize on this opportunity. With its core competencies and expertise, we anticipate significant growth in CCS revenue, projecting a low double-digit year-over-year increase.

New M&A Strategy Bolsters Growth Potential

CMG is actively seeking to acquire companies with promising, but under-utilized, proprietary products. The recent acquisition of Bluware, a leader in cloud-based deep learning solutions for subsurface analysis & Sharp Reflections a leading high-performance computing platform for seismic data processing and interpretation serves as a model for future M&A activity. With a substantial portion of the global oil, gas, and chemicals applications market comprised of smaller vendors, there is ample opportunity for CMG to continue expanding its product offerings through strategic acquisitions.

Sidecar Investment Opportunity with Constellation Directors

Mark Miller, a prominent figure in the investment community with a proven track record in acquiring vertical market software companies, joined CMG's board in 2019 and became chairman in 2022. EdgePoint, a significant shareholder holding roughly one-third of CMG, is managed by Andrew Pastor, another Constellation Software board member.

The presence of these experienced individuals from Constellation Software's board, along with their substantial shareholdings, indicates a strong potential for future growth and success.

CMG's appointment of Pramod Jain as CEO, known for his impressive track record and insightful quarterly letters, is another positive indicator. Jain's management incentives, tied to return on invested capital and growth, align the interests of insiders with those of all shareholders.

M&A

The market currently values CMG as an “oil and gas” company and not a simulation software consolidator business in our opinion, overlooking the significant and unpriced optionality introduced by its evolving M&A strategy. With the recent stock pullback and reset expectations, the setup looks appealing. CMG is well-positioned to deploy capital more aggressively, boasting $44 million in cash, no debt, and a projected $30+ million in free cash flow for the upcoming year.

If CMG consistently deploys the majority of its free cash flow into mergers and acquisitions, its evolution into an M&A-driven platform should become increasingly clear. Over the last two years, CMG has invested approximately $65 million to acquire about $46 million in revenue, implying a price-to-sales multiple of 1.4x. Given operating margins of ~26% and no debt financing, these acquisitions have yielded an estimated 18% IRR before any operational improvements. This aligns perfectly with management's stated hurdle rates from our understanding.

We estimate there are potentially over 1,000 acquisition targets in the simulation software market, encompassing various other verticals. Conservatively, CMG's five-person M&A team could realistically engage with 400-600 of these companies, aiming to acquire at least two "core" or "platform" businesses annually. We believe that once CMG successfully diversifies its capital deployment into new verticals beyond oil and gas, investors will eagerly flock to the stock.

We continue to believe that the global simulation software market is going to grow at a nice clip (12% CAGR into 2034 by some estimates). With the investments being made in cloud and high performance compute (HPC), companies built on the application layer of these investments should see increased usage as speed, accuracy and most importantly, cost savings accelerate. See attached for a white paper using engineering software simulation as an example.

In terms of the core simulation market, we note that management has increased their TAM by $500M in revenue split between the production engineering market and niche subsurface interpretation, meaning CMG would be 8.6% penetrated into their core market as at March 31, 2025.

Valuation

On a TTM basis, CMG is trading at an EV/NOPAT of ~19x, 11.5x EV/EBITDA, or 18x FCF (take your pick) which is obviously quite cheap if you believe that the M&A thesis will play out, but could still be expensive if you think there will continue to be churn within the core business in FY2026 and include limited M&A.

We've re-evaluated the core business and it's clear our initial organic growth estimates were off; it turns out customers aren't as "sticky" as we'd believed. Typically, this would signal a time to sell, as a key part of our original investment thesis is broken. However, we've decided to hold onto our shares to see how the M&A component of our thesis unfolds, as all the necessary elements are in place for its success.

Consequently, we've lowered our estimated value per share to $14 from $18 in our initial investment memo, reflecting these recent headwinds. This adjustment also brings our estimated IRR down to 19%.

Legal & Disclaimer

The information contained in this publication is not and should not be construed as investment advice, and does not purport to be and does not express any opinion as to the price at which the securities of any company may trade at any time. The information and opinions provided herein should not be taken as specific advice on the merits of any investment decision. Investors should make their own decisions regarding the prospects of any company discussed here based on such investors own review of publicly available information and should not rely on the information contained herein.

The information contained in this publication has been prepared based on publicly available information and proprietary research. The author does not guarantee the accuracy or completeness of the information provided in this document. All statements and expressions herein are the sole opinion of the author and are subject to change without notice.

Any projections, market outlooks or estimates herein are forward looking statements and are based upon certain assumptions and should not be construed to be indicative of the actual events that will occur. Other events that were not taken into account may occur and may significantly affect the returns or performance of the securities discussed herein. Except where otherwise indicated, the information provided herein is based on matters as they exist as of the date of preparation and not as of any future date, and the author undertakes no obligation to correct, update or revise the information in this document or to otherwise provide any additional materials.

The author may currently have long or short positions in the securities of certain of the companies mentioned herein, or may have such a position in the future (and therefore may profit from fluctuations in the trading price of the securities). To the extent such persons do have such positions, there is no guarantee that such persons will maintain such positions.

Neither the author nor any of its affiliates accepts any liability whatsoever for any direct or consequential loss howsoever arising, directly or indirectly, from any use of the information contained herein. In addition, nothing presented herein shall constitute an offer to sell or the solicitation of any offer to buy any security.