Brown & Brown, Inc. - Q4 2024

Transcript Notes

Summary of Financial Results and Outlook for Brown & Brown, Inc.

Financial Performance for Q4 2024:

Revenue: $1.2 billion, up 15.4% year-over-year.

Commissions & Fees: Increased 15.4% year-over-year.

Organic Revenue: Increased 13.8% year-over-year.

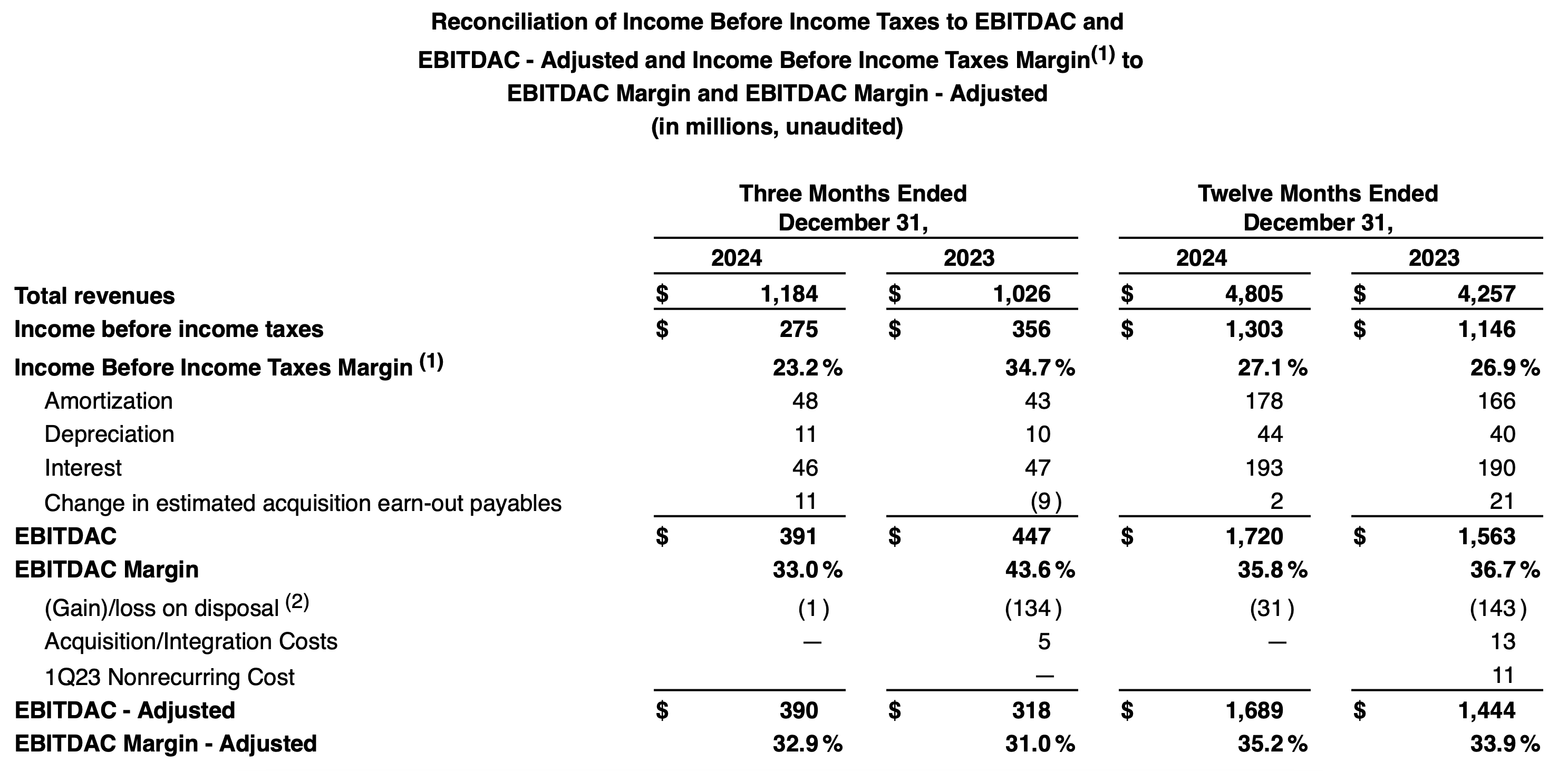

Income Before Income Taxes: $275 million, down 22.8% year-over-year (due to prior year gain on business sales).

Adjusted EBITDAC: $390 million, up 22.6% year-over-year.

Net Income: $210 million, down 21.9% year-over-year.

Diluted EPS: $0.73, down 22.3% year-over-year.

Adjusted Diluted EPS: $0.86, up 24.6% year-over-year.

Financial Performance for Full Year 2024:

Revenue (Full Year 2024): $4.8 billion, up 12.9% year-over-year.

Commissions & Fees (Full Year 2024): Up 12.1% year-over-year.

Organic Revenue (Full Year 2024): Up 10.4% year-over-year.

Income Before Income Taxes (Full Year 2024): $1.3 billion, up 13.7% year-over-year.

Adjusted EBITDAC (Full Year 2024): $1.7 billion, up 17.0% year-over-year.

Net Income (Full Year 2024): $1.0 billion, up 14.0% year-over-year.

Diluted EPS (Full Year 2024): $3.46, up 13.4% year-over-year.

Adjusted Diluted EPS (Full Year 2024): $3.84, up 18.2% year-over-year.

Economic Outlook:

The economic environment remained largely stable compared to recent quarters. Business sentiment has improved from cautious to cautiously optimistic. Company investment levels, including hiring and revenue growth, continued at a pace comparable to the second and third quarters of 2024, with no significant changes observed.

The stable economic conditions in operating markets provide a positive foundation for growth prospects in 2025 and beyond. While insurance rate increases continued across most lines, the pace of these increases is slowing compared to both last quarter and last year. Auto and casualty lines remain an exception, experiencing continued upward pricing pressure. Catastrophe (CAT) property insurance saw the most significant year-over-year change this quarter.

Insurance Pricing:

Employee benefits pricing remained consistent with recent quarters, with medical and pharmacy costs continuing to rise by 7% to 9%. This persistent upward trend, coupled with the complexities of healthcare, fuels strong demand for employee benefits consulting services.

In the admitted P&C market, rate increases moderated slightly compared to last quarter, ranging from 2% to 7% for most lines year-over-year.

Workers' compensation rates continued their downward trend, remaining flat to down 5% in most states.

Non-CAT property rate increases were flat to up 5% for the fourth quarter.

Casualty rates continued to climb for primary layers, largely driven by the magnitude of legal judgments in the U.S.

Excess casualty rates increased between 1% and 10%, consistent with recent quarters. Professional liability rates were flat to up 5% year-over-year.

E&S:

Excess & Surplus (E&S) markets, specifically CAT property, there was initial speculation in the fourth quarter that Hurricanes Helene and Milton might halt or reverse the recent downward trend in rates. However, due to the nature of the storms (primarily flooding rather than wind) and the level of insured losses, CAT property rates continued to decline throughout the quarter. Average rate decreases remained between 10% and 20%, consistent with the end of the third quarter, with an increasing number of clients experiencing decreases at or above 20%.

Segment Performance:

The retail segment saw 4.4% year-over-year organic growth, primarily due to increased contingent commissions. Total revenue in this segment increased by 9.5% year-over-year, boosted by acquisitions. BRO closed ten acquisitions in the fourth quarter of 2024, adding an estimated $137 million in annual revenue. Management noted a strong pipeline of acquisition opportunities, both domestically and internationally, and observed an increase in smaller and mid-sized deals as interest rates have declined. Commercial lines rate increases moderated to between 2% and 7% year-over-year in Q4 2024.

Management noted there will be a 100 bp headwind in Q1 2025. Retail segment has historically been a LSD-MSD organic growth business.

The programs segment delivered surprisingly strong organic growth of 38.6% year-over-year. This growth was fueled by new business, increased exposure units, and hurricane claim revenue (a one-time item). The segment's EBITDAC margin increased by 6.6% year-over-year in the fourth quarter of 2024, reaching 47.9%. This improvement resulted from more efficient expense management and, to a lesser degree, the sale of some business units.

The wholesale segment achieved 7.1% year-over-year organic growth, driven by new business and increased exposure across all lines. However, the EBITDAC margin fell by 1.4% to 25.7% due to annual performance incentives and one-time costs. In the fourth quarter of 2024, casualty lines rates rose by 5-10% while professional lines rates fell by 5-10%. Management pointed out that catastrophe property rates decreased by 10-20% during the same period.

M&A:

Successful quarter for mergers and acquisitions, acquiring 10 companies with combined annual revenues of $137 million. Largest acquisition was Quintes, which strengthens position in the Dutch market and provides significant growth potential. The M&A market remains competitive, particularly for quality businesses. With decreasing interest rates, observing increased activity from financial sponsors, especially in the small and mid-size deal segments.

In the Netherlands, a substantial number of policies are placed in the first quarter of the year. As a result, BRO will record approximately 60% of Quintes’ annual revenues in the first quarter with the remaining revenues recognized fairly evenly over the following three quarters. From a margin perspective, this will improve Q1 margins and will unfavourably impact the margins in the other quarters.

Private equity firms are attracted to insurance service companies due to their capital-light, lean staffing, high-margin, and contractually secured cash flow business model.

All the bigger deals in 2024 were done by PE firms for the most part.

Continue to look at prices paid by PE firms in a hardening market.

BRO is staying conservatively financed and is paying down debt, giving them optionality to do a big deal if the cultural fit is right.

Organic Growth:

Strong new business generation across all three divisions – record levels of new business in 2024. Confident in continued new business growth due to existing and newly developed capabilities (both built and acquired). Effective cross-divisional collaboration enables leveraging these capabilities for the benefit of all customers.

Miscellaneous Notes:

We now have a clearer picture of when claims will be processed and how severe they are. As a result, we expect to recognize between $14 million and $18 million in revenue during the first half of 2025. Most of this will be recorded in the first quarter, primarily related to flood claim processing revenue from Hurricanes Helene and Milton.

Corporate segment did $11 million of negative EBITDA in the quarter. Andy noted some one-off costs. “We just had some one-off costs in there in the fourth quarter, nothing real unusual in nature. So those can always kind of move around by quarters and by years, but nothing unusual.”

Note to self: Go check the notes disclosures on these for curiosity sake, not material though.

Powell Brown acknowledged that his response was speculative when asked about the rebuild in California and if there was enough contractors, but based on the extent of the damage, he believes there simply won't be enough contractors to meet the overwhelming demand for rebuilding. He also noted that he'd heard that obtaining a building permit could take as long as 18 months. Therefore, he feels it's crucial for the Governor and other officials to find a more efficient way to expedite the rebuilding process. He suggested considering a large-scale initiative, similar in scope to the Marshall Plan, to accelerate construction.

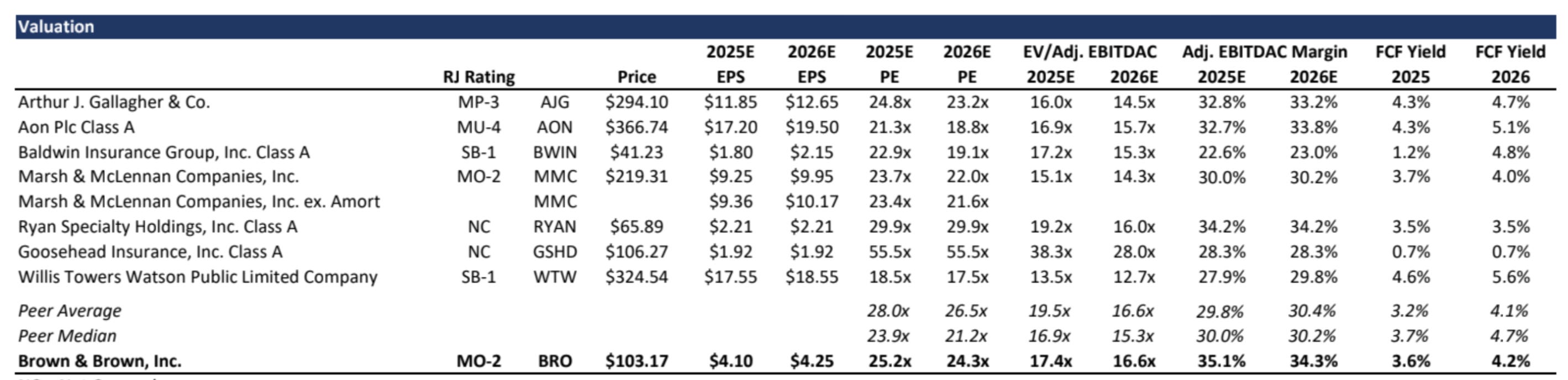

Simple Valuation Metrics:

Insurance brokers are expected to maintain high valuations in 2025 and 2026. This is due to their consistent and recurring cash flows, minimal capital expenditure needs, and their growing importance within the insurance industry's distribution network.

Smaller insurance brokers are gaining market share at the expense of larger, multinational companies. As a result, these large-cap players are increasingly relying on acquisitions to recover their lost market share.

this should play in BRO’s favour as they continue to consolidate smaller players and are leading the pack in terms of organic growth.

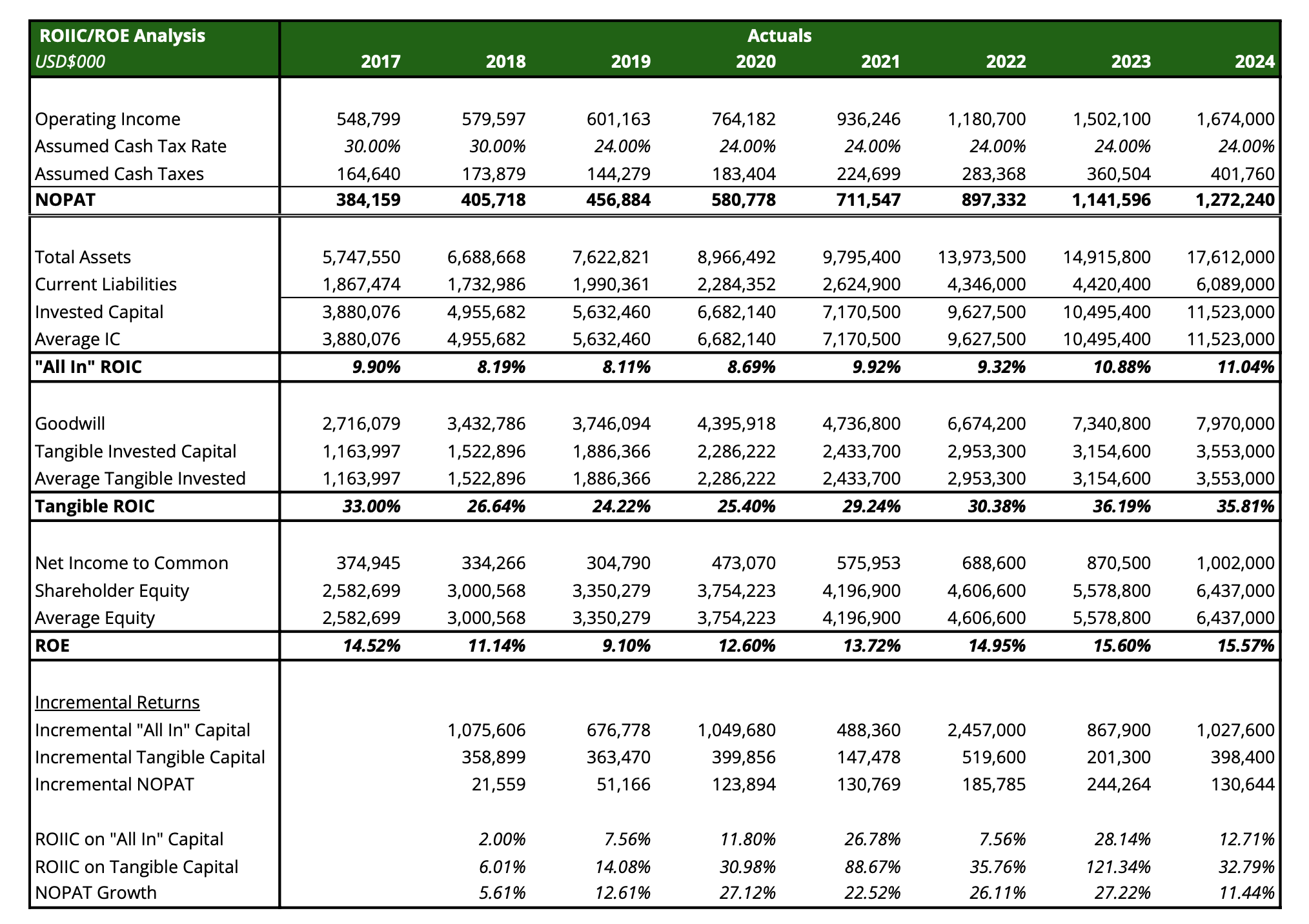

ROIIC/ROE Checkup: